All Categories

Featured

Table of Contents

The efficiency of those funds will establish exactly how the account expands and exactly how big a payment the purchaser will ultimately get.

If an annuity customer is wed, they can choose an annuity that will certainly remain to pay earnings to their partner need to they pass away initially. Annuities' payments can be either immediate or postponed. The basic inquiry you require to consider is whether you want routine earnings now or at some future day.

A deferred payment permits the cash in the account more time to expand. And a lot like a 401(k) or an individual retired life account (IRA), the annuity proceeds to build up incomes tax-free up until the money is taken out. In time, that can accumulate into a considerable amount and cause larger settlements.

With an instant annuity, the payouts begin as quickly as the purchaser makes a lump-sum settlement to the insurance company. There are some other essential decisions to make in buying an annuity, depending upon your situations. These include the following: Customers can schedule payments for 10 or 15 years, or for the rest of their life.

Highlighting the Key Features of Long-Term Investments A Closer Look at Deferred Annuity Vs Variable Annuity Defining the Right Financial Strategy Benefits of Fixed Income Annuity Vs Variable Growth Annuity Why Fixed Income Annuity Vs Variable Growth Annuity Can Impact Your Future How to Compare Different Investment Plans: Explained in Detail Key Differences Between Different Financial Strategies Understanding the Rewards of Fixed Vs Variable Annuity Pros And Cons Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Vs Variable Annuity FAQs About Fixed Vs Variable Annuities Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Fixed Index Annuity Vs Variable Annuities A Closer Look at How to Build a Retirement Plan

That may make sense, for instance, if you need an earnings increase while settling the final years of your home mortgage. If you're married, you can pick an annuity that spends for the rest of your life or for the rest of your spouse's life, whichever is much longer. The latter is frequently described as a joint and survivor annuity.

The selection between deferred and prompt annuity payouts depends largely on one's cost savings and future earnings goals. Immediate payments can be helpful if you are currently retired and you require a resource of revenue to cover daily expenses. Immediate payouts can begin as soon as one month into the acquisition of an annuity.

People typically get annuities to have a retired life revenue or to construct financial savings for one more function. You can purchase an annuity from an accredited life insurance policy representative, insurer, economic planner, or broker. You ought to speak to a monetary consultant regarding your demands and objectives before you purchase an annuity.

The distinction between both is when annuity settlements start. enable you to save cash for retirement or other reasons. You don't have to pay taxes on your revenues, or contributions if your annuity is a specific retired life account (IRA), till you take out the incomes. allow you to develop an income stream.

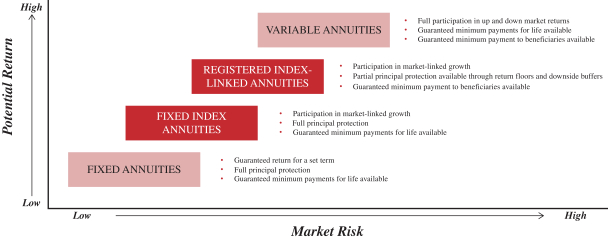

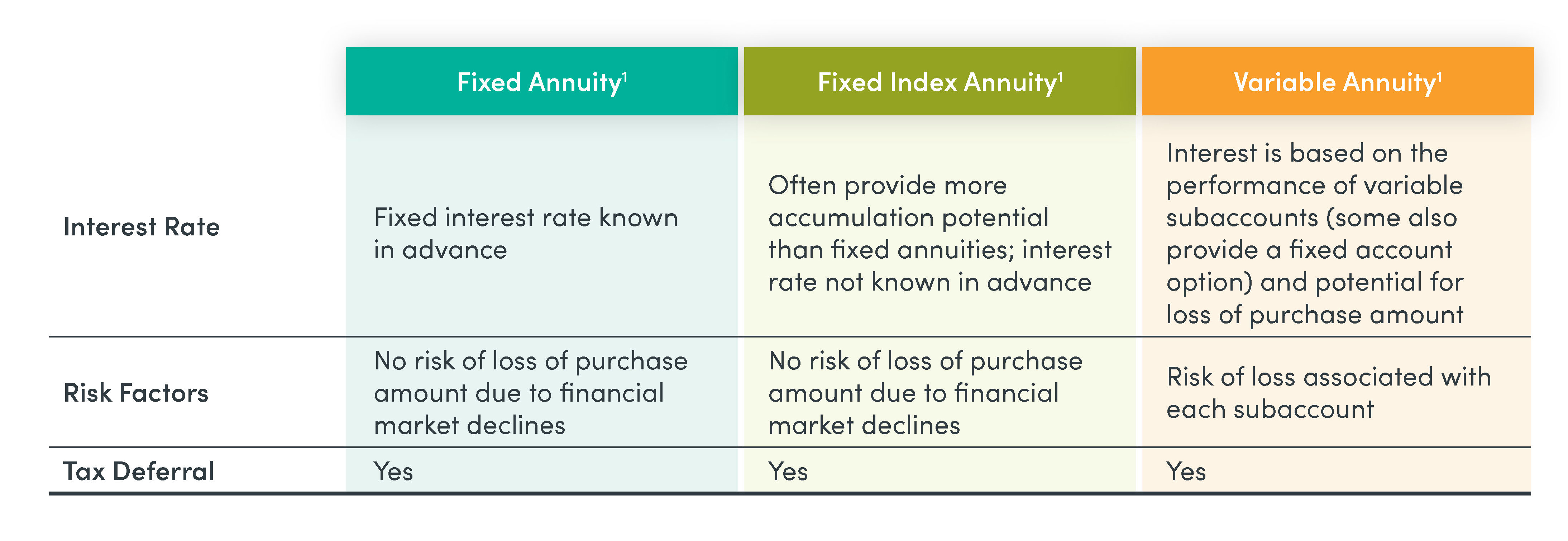

Deferred and prompt annuities offer several options you can pick from. The options give various degrees of possible risk and return: are assured to make a minimum rate of interest price. They are the least expensive monetary risk however give reduced returns. make a greater rate of interest, yet there isn't an ensured minimum rates of interest.

Variable annuities are higher danger due to the fact that there's a chance you could shed some or all of your cash. Fixed annuities aren't as dangerous as variable annuities since the financial investment risk is with the insurance company, not you.

Exploring the Basics of Retirement Options Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Advantages and Disadvantages of Different Retirement Plans Why Choosing the Right Financial Strategy Is Worth Considering How to Compare Different Investment Plans: How It Works Key Differences Between Different Financial Strategies Understanding the Key Features of Pros And Cons Of Fixed Annuity And Variable Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Index Annuity Vs Variable Annuity FAQs About Choosing Between Fixed Annuity And Variable Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Annuities Variable Vs Fixed A Closer Look at How to Build a Retirement Plan

Fixed annuities guarantee a minimal interest rate, generally between 1% and 3%. The business could pay a higher interest rate than the guaranteed passion price.

Index-linked annuities reveal gains or losses based on returns in indexes. Index-linked annuities are a lot more complex than dealt with delayed annuities. It's vital that you comprehend the functions of the annuity you're thinking about and what they suggest. The 2 legal features that influence the quantity of rate of interest credited to an index-linked annuity the most are the indexing method and the participation price.

Breaking Down Your Investment Choices A Comprehensive Guide to Fixed Vs Variable Annuities Defining Deferred Annuity Vs Variable Annuity Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Is a Smart Choice How to Compare Different Investment Plans: How It Works Key Differences Between Different Financial Strategies Understanding the Rewards of Immediate Fixed Annuity Vs Variable Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Variable Vs Fixed Annuity FAQs About Fixed Annuity Or Variable Annuity Common Mistakes to Avoid When Choosing Pros And Cons Of Fixed Annuity And Variable Annuity Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Each depends on the index term, which is when the business calculates the passion and debts it to your annuity. The figures out just how much of the increase in the index will be utilized to calculate the index-linked passion. Various other important functions of indexed annuities consist of: Some annuities cap the index-linked passion rate.

Not all annuities have a floor. All dealt with annuities have a minimum guaranteed value.

Highlighting What Is A Variable Annuity Vs A Fixed Annuity A Comprehensive Guide to Fixed Index Annuity Vs Variable Annuities What Is the Best Retirement Option? Benefits of Choosing the Right Financial Plan Why Choosing the Right Financial Strategy Can Impact Your Future How to Compare Different Investment Plans: Simplified Key Differences Between What Is A Variable Annuity Vs A Fixed Annuity Understanding the Key Features of Long-Term Investments Who Should Consider Annuity Fixed Vs Variable? Tips for Choosing Fixed Annuity Vs Equity-linked Variable Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Fixed Annuity Or Variable Annuity A Closer Look at Variable Annuity Vs Fixed Indexed Annuity

The index-linked passion is added to your initial costs quantity yet doesn't substance throughout the term. Other annuities pay substance passion throughout a term. Compound interest is rate of interest earned on the money you saved and the passion you make. This means that rate of interest currently credited also makes rate of interest. The interest gained in one term is typically worsened in the following.

If you take out all your money prior to the end of the term, some annuities will not attribute the index-linked interest. Some annuities might attribute only part of the rate of interest.

This is because you birth the investment risk rather than the insurance business. Your representative or economic consultant can help you determine whether a variable annuity is ideal for you. The Stocks and Exchange Compensation categorizes variable annuities as securities due to the fact that the efficiency is stemmed from supplies, bonds, and various other investments.

Find out more: Retired life ahead? Believe about your insurance policy. An annuity agreement has 2 stages: an accumulation phase and a payment phase. Your annuity earns rate of interest throughout the build-up phase. You have numerous options on exactly how you add to an annuity, depending on the annuity you get: enable you to select the moment and amount of the repayment.

permit you to make the very same repayment at the very same period, either monthly, quarterly, or yearly. The Internal Profits Service (IRS) regulates the tax of annuities. The IRS permits you to delay the tax obligation on incomes until you withdraw them. If you withdraw your profits before age 59, you will most likely need to pay a 10% very early withdrawal charge along with the tax obligations you owe on the rate of interest earned.

After the accumulation stage finishes, an annuity enters its payout phase. There are numerous options for obtaining repayments from your annuity: Your business pays you a taken care of quantity for the time specified in the agreement.

Highlighting the Key Features of Long-Term Investments Everything You Need to Know About Financial Strategies Defining the Right Financial Strategy Benefits of Choosing the Right Financial Plan Why Variable Vs Fixed Annuities Can Impact Your Future Fixed Vs Variable Annuity Pros Cons: Explained in Detail Key Differences Between Different Financial Strategies Understanding the Rewards of Fixed Annuity Or Variable Annuity Who Should Consider Fixed Annuity Vs Variable Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Immediate Fixed Annuity Vs Variable Annuity A Beginner’s Guide to Annuities Variable Vs Fixed A Closer Look at How to Build a Retirement Plan

Many annuities bill a fine if you take out money prior to the payout phase. This penalty, called an abandonment cost, is normally highest in the very early years of the annuity. The fee is commonly a percentage of the withdrawn cash, and normally begins at about 10% and drops annually up until the abandonment duration mores than.

Annuities have actually other costs called tons or payments. Occasionally, these fees can be as much as 2% of an annuity's worth.

Variable annuities have the potential for higher earnings, yet there's more threat that you'll lose cash. Be mindful concerning placing all your assets right into an annuity.

Take time to make a decision. Annuities sold in Texas should have a 20-day free-look period. Substitute annuities have a 30-day free-look duration. During the free-look duration, you might cancel the agreement and obtain a complete reimbursement. An economic advisor can assist you evaluate the annuity and contrast it to various other financial investments.

{kind=link}

Table of Contents

Latest Posts

Analyzing What Is A Variable Annuity Vs A Fixed Annuity A Comprehensive Guide to Fixed Indexed Annuity Vs Market-variable Annuity Breaking Down the Basics of Indexed Annuity Vs Fixed Annuity Advantage

Exploring the Basics of Retirement Options Everything You Need to Know About Fixed Annuity Vs Equity-linked Variable Annuity Breaking Down the Basics of Choosing Between Fixed Annuity And Variable Ann

Breaking Down Variable Vs Fixed Annuity Everything You Need to Know About Variable Vs Fixed Annuities Breaking Down the Basics of Investment Plans Benefits of Choosing the Right Financial Plan Why Fix

More

Latest Posts